Why Your Levered Single-Stock ETF Is Quietly Underperforming

In a recent research paper titled “Returns to Constant Leverage Strategies: General Principles and Application to Levered Single-Stock ETFs,” Professor Hendrik Bessembinder of Arizona State University provides a deep dive into the mechanics and risks of the rapidly growing levered single-stock ETF (LSS-ETF) market.

Since their introduction in 2022, these products have surged in popularity, reaching over $18 billion in market capitalization by mid-2025. However, Bessembinder’s analysis reveals that these “lottery-like” investments often come with structural performance drags that most retail investors may not fully realize.

Related reading:-Triple Leveraged Trading Strategy

The Performance Gap: Rebalancing vs. Friction

Bessembinder’s research highlights that actual LSS-ETFs frequently underperform a simple levered buy-and-hold benchmark.

- Monthly Underperformance: On average, long levered single-stock ETFs underperform their benchmarks by 0.79% per month.

- Decomposing the Loss: This shortfall is driven by two main factors: daily rebalancing trades (accounting for 0.26%) and frictional costs like management fees, trading execution, and loan margins (accounting for 0.53%).

- Cost Asymmetry: Interestingly, the study found that frictional costs are higher for long leverage funds, while rebalancing costs are significantly higher for inverse (short) funds.

Debunking the “Volatility Decay” Myth

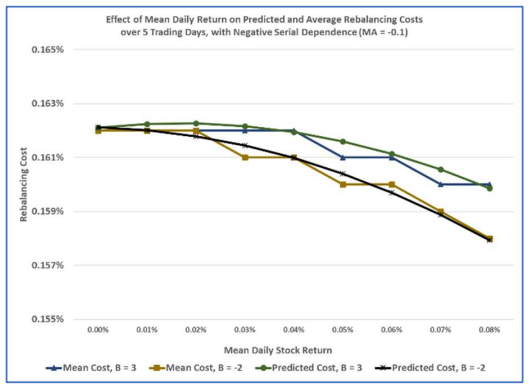

While investors often hear about “volatility decay,” Bessembinder clarifies that volatility itself isn’t the only enemy. Instead, the impact depends on serial correlation, or how a stock’s price movements relate to one another over time.

- The Momentum Benefit: If a stock has high positive serial correlation (meaning it trends in one direction), high volatility can actually improve levered returns.

- The Reversal Trap: Rebalancing costs become painful when stocks experience return reversals – common in high-volatility periods. During these times, the ETF is forced to “buy high and sell low” to maintain its constant leverage ratio.

The “Winner-Take-All” Skewness

One of the most striking conclusions of the paper is the extreme positive skewness of these funds. Because returns compound over time, a few massive “home run” outcomes pull up the average (mean) return, while the typical (median) experience is much worse.

- Negative Median Returns: In a hypothetical 50-year study of 3x levered funds, the mean annual return was a staggering 29.20%, yet the median return was negative 13.31%.

- The Practical Reality: This means that more than half the time, investors in these triple-levered strategies would have lost money, even if the average market return appeared highly positive.

The Risk of a Total “Wipeout”

Because individual stocks are far more volatile than diversified indices like the S&P 500, LSS-ETFs carry a non-trivial risk of a 100% loss.

- Target Returns Below -100%: Bessembinder calculates that if 3x levered funds had existed for all stocks since 1973, a daily target return of -100% or worse would have occurred 2.8 times per trading day on average.

- Zero-Sum Losses: While investors have limited liability and cannot lose more than their initial investment, these “excess losses” must be absorbed by the fund sponsor or swap counterparties.

Final Takeaway

For many, LSS-ETFs are the “extreme sports” of the investing world. While they offer the potential for massive short-term gains, the structural costs of daily rebalancing and the mathematical reality of skewness mean that the longer you hold them, the more likely you are to underperform, or even face a total wipeout.

Analogy for the Road: Think of a levered single-stock ETF like a high-performance race car explicitly designed for a straight track. If the track is straight (trending markets), the car’s turbo-charged engine gets you to the finish line faster than anyone else.

However, if the track is full of sharp S-curves and hairpins (volatility with reversals), the driver must constantly brake and accelerate. This doesn’t just burn more fuel (frictional costs); it wears down the engine so much that the car might break down before reaching the finish line, even if it was the fastest car on paper