How to Backtest a Futures Strategy: The Ultimate Step-by-Step Guide for 2026

Backtesting a futures strategy is one of those essential practices that can make the difference between consistent gains and unexpected losses in the fast-paced world of trading.

Imagine having a roadmap that shows how your ideas would have played out in real market conditions without risking a single dollar. That’s the beauty of backtesting—it’s like a time machine for your trading plans.

In this comprehensive guide, we’ll walk through everything you need to know to get started, from the basics to more advanced considerations, all while keeping things straightforward and practical. Whether you’re new to futures or looking to refine your approach, this article aims to equip you with the knowledge to test strategies effectively and confidently.

What Is Backtesting in Futures Trading?

Backtesting in futures trading refers to the process of applying a set of trading rules to historical market data to evaluate how the strategy would have performed over time. Unlike stocks or forex, futures contracts have unique characteristics, such as expiration dates and leverage, which make backtesting particularly valuable for understanding potential outcomes.

By simulating trades based on past price movements, volume, and other indicators, traders can gain insights into profitability, risk levels, and overall viability without exposing capital to live markets.

This method has roots in quantitative analysis, where data-driven decisions replace gut feelings. In futures, where contracts like those for commodities, indices, or currencies roll over periodically, backtesting helps identify patterns that might repeat. It’s not about predicting the future with certainty, markets are unpredictable, but about building a foundation of evidence.

Many successful traders swear by it because it reveals flaws early, saving time and money. For instance, a strategy that looks promising on paper might show consistent drawdowns during volatile periods, prompting adjustments before real trading begins.

Why Should You Backtest Your Futures Strategy?

Backtesting your futures strategy provides a reality check that can prevent costly mistakes in live trading. Without it, you’re essentially flying blind, relying on hope rather than historical evidence. By running simulations on past data, you can measure key metrics like win rate, risk-reward ratio, and maximum drawdown, which offer a clearer picture of what to expect.

This is especially crucial in futures markets, where high leverage can amplify both gains and losses, and external factors like economic reports or geopolitical events can swing prices dramatically.

Moreover, backtesting builds confidence. When you’ve seen a strategy hold up across different market conditions—bullish, bearish, or sideways—you’re more likely to stick with it during tough times. It also encourages discipline, as the process forces you to define clear entry and exit rules upfront. In a field where emotions often lead to impulsive decisions, this objectivity is a game-changer.

Studies and trader experiences shared across platforms highlight that strategies without thorough testing often fail when faced with real-world slippage or unexpected volatility. Ultimately, it’s about stacking the odds in your favor, turning trading from a gamble into a calculated endeavor.

Essential Data for Backtesting Futures Strategies

To backtest a futures strategy effectively, you need high-quality historical data that mirrors real market conditions as closely as possible. This includes price data—open, high, low, close—for the specific futures contracts you’re interested in, along with volume and time stamps.

For accuracy, tick-by-tick data is ideal, especially for intraday strategies, as it captures every trade and quote. Many platforms provide this, but ensure the data spans multiple years to cover various market cycles, avoiding biases from short-term anomalies.

Beyond prices, incorporate factors like contract specifications, including tick size, margin requirements, and rollover dates. Economic calendars can add context, helping simulate how news events might impact trades. Clean data is key; watch for gaps or errors that could skew results.

Sources like CME Group or dedicated providers offer reliable datasets, often with adjustments for continuous contracts to smooth out expirations. Remember, the goal is realism—poor data leads to misleading outcomes, so invest time in sourcing and verifying it.

How to Handle Continuous Futures Contracts in Backtesting

Handling continuous futures contracts in backtesting is a critical step to avoid artificial price jumps that can distort your results. Futures contracts expire periodically, so to create a seamless historical series, you stitch together individual contracts into one continuous stream. This process, known as rolling, adjusts for differences in prices between expiring and new contracts due to contango or backwardation.

Common methods include the backwards ratio adjustment, where past prices are scaled to match the current contract, preserving percentage changes. Another approach is the first-of-the-month roll, switching contracts at a fixed date to minimize disruptions.

In software like NinjaTrader, use merge policies such as MergeBackAdjusted to automate this. Without proper handling, your backtest might show unrealistic profits or losses at roll points. Always test your continuous series for smoothness before running full simulations to ensure the data reflects true market behavior.

Step-by-Step Guide to Backtesting a Futures Strategy

Starting with a clear hypothesis is the foundation of any backtest. Define your strategy’s rules precisely: what signals trigger entries, like a moving average crossover or RSI oversold condition? Set exits based on profit targets, stop-losses, or time-based rules. Choose a futures market, such as crude oil or S&P 500 minis, and a timeframe that aligns with your trading style—daily for swing trades or minutes for scalping.

Next, gather and prepare your data, ensuring it’s adjusted for continuous contracts. Input your rules into backtesting software, incorporating realistic elements like commissions and slippage. Run the simulation over a substantial period, say five to ten years, to capture diverse conditions.

Analyze the output: look at net profit, win percentage, and drawdowns. Iterate by tweaking parameters, but avoid over-optimization. Finally, validate with out-of-sample data to check for robustness. This systematic approach turns abstract ideas into testable plans.

What Is Backtesting & How to Backtest a Trading Strategy Using Python

Best Software and Tools for Backtesting Futures

Choosing the right software can streamline your backtesting process for futures strategies. AmiBroker stands out as a powerful desktop tool renowned for its speed and flexibility in handling futures. It offers true portfolio-level backtesting, blazing-fast optimization even on large datasets, and dedicated futures mode that properly accounts for margin deposits, point values, and contract specifications to deliver realistic simulations.

With its AFL (AmiBroker Formula Language) scripting, you can create highly customized indicators, strategies, and metrics, making it ideal for serious traders who want deep control over position sizing, slippage emulation, custom commissions, and walk-forward testing. While it has a learning curve for programming, its efficiency in testing across multiple symbols and timeframes makes it a favorite among quantitative-focused futures traders.

TradeStation is another excellent choice, particularly for those who value an integrated platform with strong historical data access and seamless transition from backtesting to live execution. It excels with extensive decades of data for U.S. and Eurex futures, allowing thorough validation of ideas against real market conditions.

Using its EasyLanguage programming (which is relatively straightforward and human-readable), you can build, test, and optimize strategies without advanced coding skills in many cases. Features like Portfolio Maestro enable group strategy evaluation across baskets of symbols, while options for intrabar order generation, backtest resolution adjustments, slippage/commission settings, and detailed performance reports provide precise insights.

TradeStation’s simulator and automation capabilities make it especially appealing for futures traders looking to refine approaches before going live.

Each platform brings distinct advantages—AmiBroker for raw speed, customization, and portfolio depth, TradeStation for user-friendly strategy development and broad futures data support. Pick based on your comfort with scripting, desired level of integration with live trading, cost considerations, and specific futures needs. Both remain highly regarded options in the futures community for reliable, professional-grade backtesting.

Common Mistakes to Avoid When Backtesting Futures Strategies

One frequent pitfall in backtesting futures strategies is overfitting, where you tweak parameters too much to fit historical data perfectly, only for the strategy to fail in live markets. This creates illusionary profits. To counter it, use out-of-sample testing and keep rules simple.

Look-ahead bias sneaks in when your strategy uses future information unavailable at the time, like closing prices for intraday decisions. Always ensure signals rely only on past data. Ignoring transaction costs, slippage, and commissions inflates results—futures have margins and fees that add up.

Using insufficient data leads to time-period bias; test across bull, bear, and flat markets. Hindsight bias, where you interpret charts knowing outcomes, distorts manual tests—stick to rules blindly. Survivorship bias ignores delisted contracts, skewing optimism. By recognizing these, you can refine your process for more reliable insights.

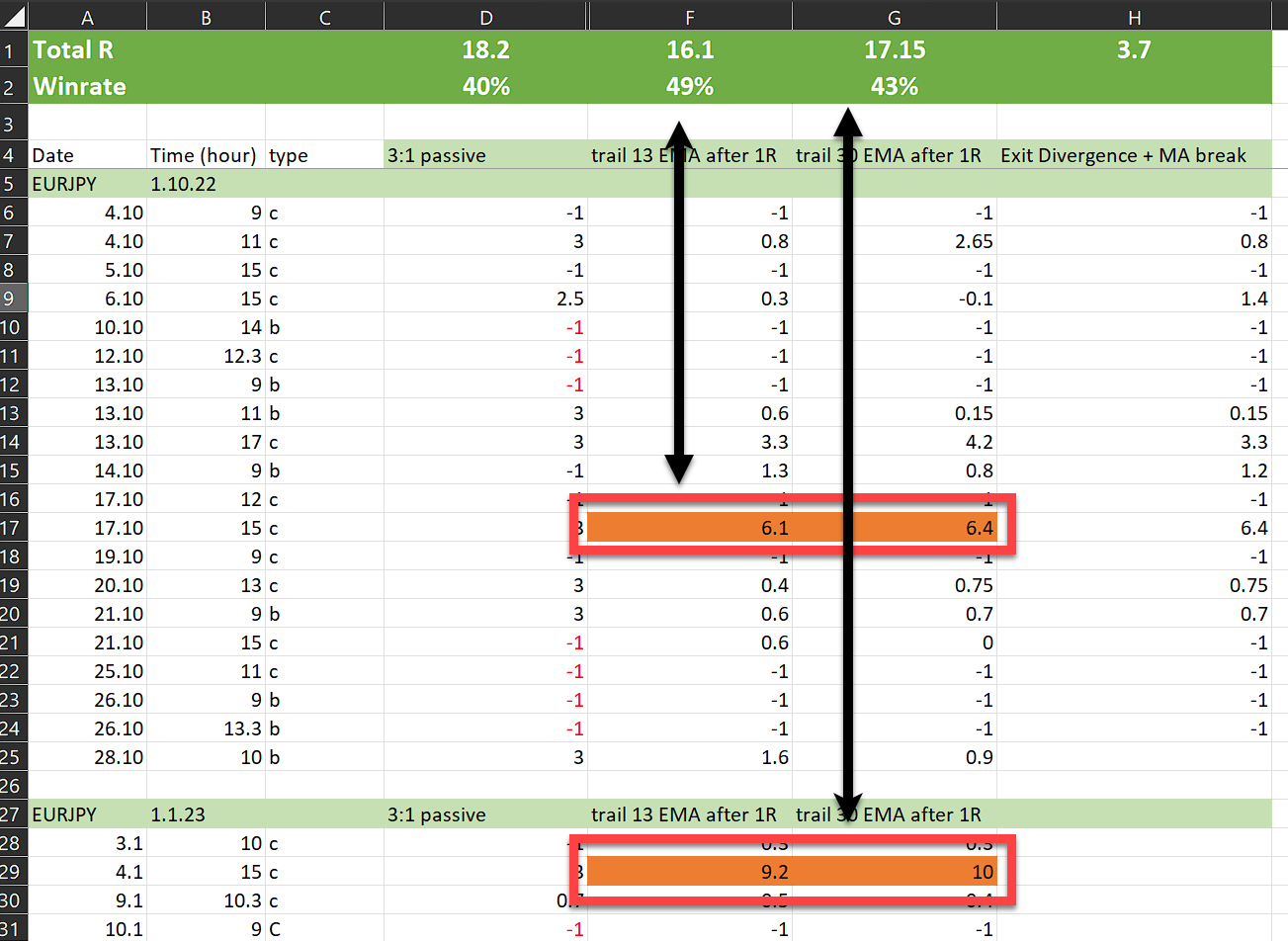

How to Interpret and Analyze Backtesting Results

Interpreting backtesting results goes beyond net profit; focus on risk-adjusted metrics for a balanced view. The Sharpe ratio measures returns relative to volatility—higher is better, indicating smoother performance. Maximum drawdown shows the largest peak-to-trough drop, helping gauge tolerance for losses.

Win rate alone misleads; a 40% win rate with high reward-to-risk can outperform a 70% strategy with small gains. Examine equity curves for steady growth, not sharp spikes. Compare against benchmarks like buy-and-hold to see added value. Factor in futures-specific elements, like roll yields. If results seem too good, check for biases. Use Monte Carlo simulations to test robustness under varied scenarios. This thorough analysis turns raw data into actionable wisdom.

The Ultimate Guide to Backtesting

Advanced Techniques in Futures Backtesting

For those ready to elevate their game, advanced techniques in futures backtesting include walk-forward optimization, where you periodically re-optimize parameters on rolling windows to mimic real adaptation. This reduces overfitting risks.

Incorporate machine learning for pattern recognition, using libraries like scikit-learn in Python to predict outcomes based on features. Multi-asset backtesting tests correlations across futures like oil and currencies. Stress testing simulates extreme events, like 2008 crashes, to assess resilience. Event-driven backtests factor in news impacts. These methods provide deeper insights, but require computational power and caution against complexity that obscures core logic.

Backtesting vs. Forward Testing: What’s the Difference?

Backtesting uses historical data to simulate past performance, offering quick feedback on strategy viability. It’s efficient but limited by data quality and inability to capture live emotions or slippage fully.

Forward testing, or paper trading, applies the strategy in real-time without real money, bridging the gap to live execution. It reveals issues like order fills in volatile futures markets that backtests miss. While backtesting is retrospective, forward testing is prospective, validating under current conditions. Both are essential: backtest to refine, forward test to confirm before going live. This combo minimizes surprises.

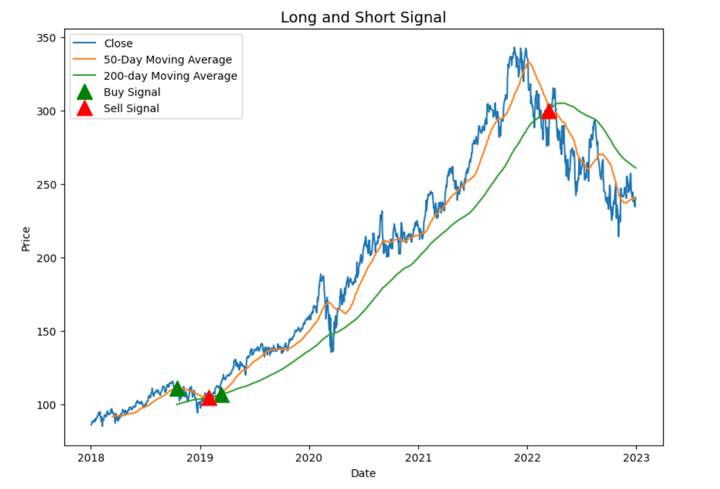

Case Study: Backtesting a Simple Moving Average Crossover Strategy for Futures

Consider a basic moving average crossover strategy on crude oil futures. The rules: buy when the 50-day SMA crosses above the 200-day SMA; sell when it crosses below. Using continuous contracts from 2015 to 2025, the backtest might show a 45% win rate with a 1.8 risk-reward ratio, yielding moderate profits but significant drawdowns during 2020’s volatility.

Adjusting for slippage and commissions reduces net gains by 15%, highlighting realism’s importance. Out-of-sample testing from 2023 onward confirms consistency. This case illustrates how a simple strategy can work in trending markets but falter in ranges, prompting additions like filters. Lessons learned: trends drive success, but diversification helps.

Our Strategy Shop for Futures Strategies

If you’re looking for ready-to-use or inspiration-ready futures strategies that fit nicely with tools like AmiBroker or TradeStation or any other platform or even strategies in plain English, check out our futures strategy shop.

We’ve put together a curated selection of tested futures approaches—everything from trend-following setups and breakout plays to mean-reversion ideas and simple spread trades. Each one comes with clear rules, backtest notes where available, and suggestions on how to implement them in your preferred platform.

We keep things practical and straightforward: no hype, just solid ideas built from real market behavior that you can tweak to match your style and risk level. Whether you’re new to futures and want something straightforward to start with, or you’re more experienced and looking for fresh concepts to refine, there’s likely something here that clicks for you.

Browse the shop at your own pace, download what interests you, and always run your own backtests first—that’s the best way to make any strategy truly yours. We’re here to help make futures trading feel a bit more approachable and effective, one solid idea at a time.

In wrapping up, backtesting a futures strategy is a powerful tool that demands care, quality data, and an objective mindset. By following these steps and avoiding common traps, you’ll be better positioned to navigate markets with confidence. Remember, no test guarantees future success, but thorough preparation certainly improves your chances. Start small, learn from each run, and keep evolving your approach—happy trading!