Adaptive Grid Trading Strategy: ATR Percentile-Based Grid Trading for Crypto Markets

The Adaptive Grid Trading Strategy enhances traditional grid trading by dynamically adjusting grid deployment using ATR Percentile ranking, a normalized volatility metric. Designed for cryptocurrency markets, it enables consistent application across assets like Bitcoin (BTC), Ethereum (ETH), and Solana (SOL) without asset-specific tuning. By activating grids only during high relative volatility regimes, the strategy improves capital efficiency and mitigates risks associated with static grid parameters.

What Is the Adaptive Grid Trading Strategy?

The Adaptive Grid Trading Strategy is a systematic cryptocurrency trading approach that combines classical grid trading mechanics with volatility normalization using ATR Percentile ranking.

Instead of relying on fixed volatility thresholds or asset-specific configurations, the strategy evaluates current volatility relative to an asset’s own historical volatility distribution. This allows identical trading rules to be applied consistently across multiple cryptocurrencies with vastly different volatility profiles.

Key Takeaways

- Adaptive grid trading uses ATR percentile volatility

- ATR percentile normalizes volatility across cryptocurrencies

- Grid trading activates during high volatility regimes

- Grid spacing adjusts using ATR-based intervals

- Strategy exits during low volatility conditions

- Same parameters work across multiple crypto assets

- Improves capital efficiency in crypto portfolios

- Best suited for high-volatility range markets

Primary objectives:

- Activate grid trading during high relative volatility

- Avoid or exit grids during low relative volatility

- Eliminate manual per-asset parameter optimization

- Improve capital efficiency in multi-asset portfolios

How It Works

At its core, the strategy uses Average True Range (ATR) as a volatility input and converts it into a percentile rank based on historical data.

Instead of comparing raw ATR values across assets—which is ineffective due to differing volatility baselines—the strategy compares where current volatility sits within each asset’s own historical range.

- A high ATR Percentile signals elevated volatility relative to history

- A low ATR Percentile signals compressed volatility

Grid trading is activated, adjusted, or deactivated based on these percentile regimes.

Step-by-Step Process / Method

1. Calculate ATR

- ATR is typically calculated using a 14-period setting

- It measures true price range, accounting for gaps and intrabar movement

2. Rank ATR Using a Historical Lookback

- Collect ATR values over 100–200 bars

- Rank the current ATR within this historical distribution

ATR Percentile Formula:ATR Percentile=(Total historical ATR valuesHistorical ATR values≤Current ATR)×100

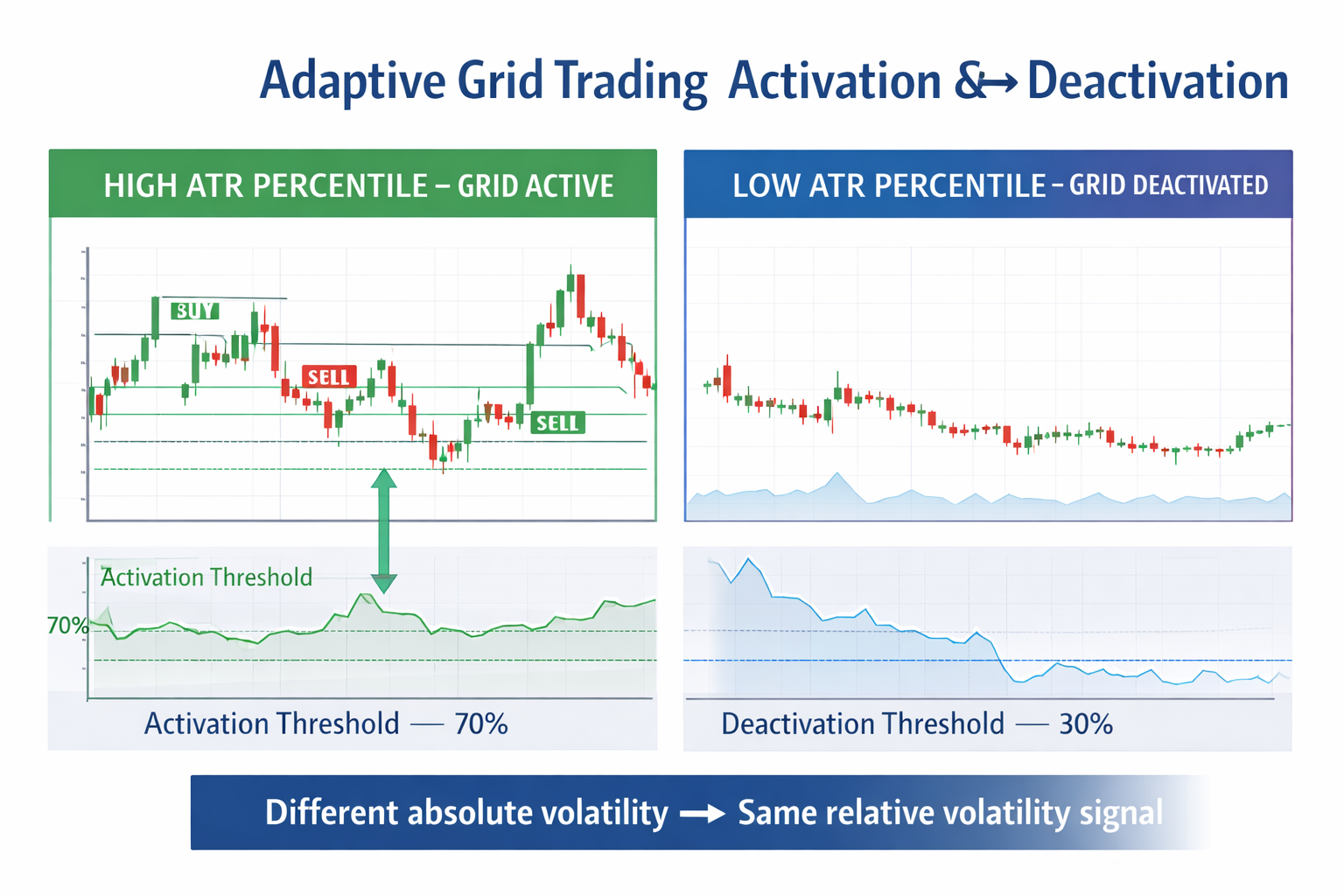

3. Determine Volatility Regime

- High volatility: ATR Percentile ≥ 70–80

- Low volatility: ATR Percentile ≤ 25–30

- Neutral zone: 30–70

4. Activate Grid (High Percentile)

- Grid is deployed only when ATR Percentile exceeds the activation threshold

- Optional filters may confirm range-bound conditions

5. Construct Grid Using ATR-Based Spacing

- Grid interval = ATR × multiplier (typically 0.10–0.20)

- Spacing widens automatically in higher volatility regimes

- Orders are placed symmetrically around the reference price

6. Monitor and Adjust Dynamically

- Grid parameters update as ATR Percentile evolves

- Spacing expands in high volatility and contracts as volatility falls

7. Deactivate and Exit

- Grid exits when ATR Percentile drops below the low-volatility threshold

- All open positions are unwound and pending orders canceled

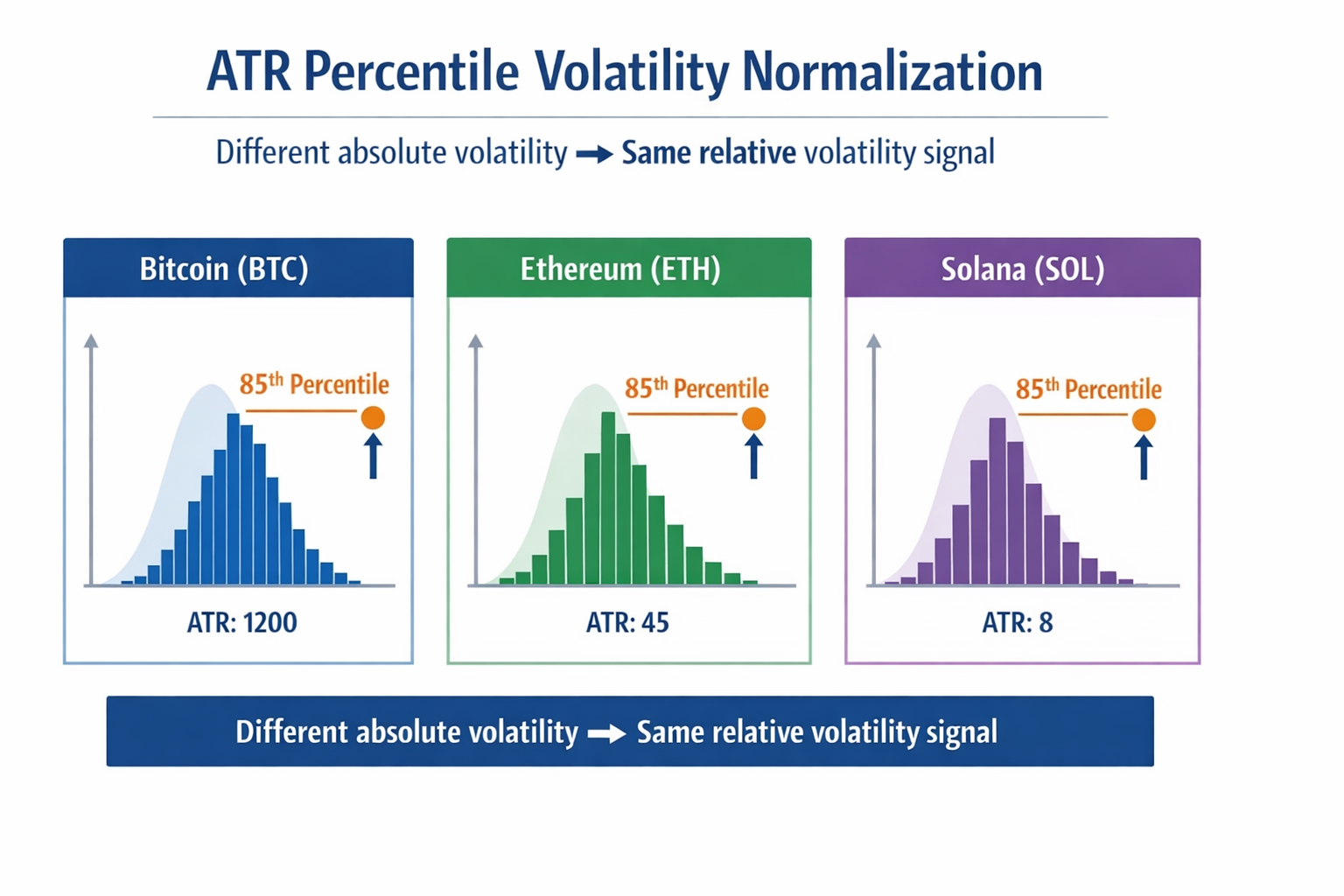

Example: Cross-Asset Volatility Normalization

Consider the following scenario:

- BTC ATR: 2% → 85th percentile

- SOL ATR: 8% → 85th percentile

Despite the large difference in absolute volatility, both assets are experiencing equally elevated relative volatility.

Result:

- The strategy activates grids on both assets using the same rules

- No asset-specific tuning is required

- Risk exposure remains consistent across the portfolio

Key Benefits

- Volatility normalization across assets

- No per-coin parameter optimization

- Reduced idle capital in low-volatility markets

- Improved capital efficiency

- Consistent behavior across BTC, ETH, and SOL

- Automatic adaptation to changing market regimes

Limitations or Risks

- Lag risk: Percentile ranking may react slowly to sudden volatility shifts

- Trend risk: Persistent directional moves can challenge grid assumptions

- Parameter sensitivity: Poor lookback or threshold selection degrades performance

- Whipsaw exposure: Rapid volatility reversals can increase execution noise

Common Mistakes

- Using absolute ATR thresholds instead of percentiles

- Activating grids in low volatility regimes

- Overly short lookback periods that introduce noise

- Ignoring trend breakouts while grids are active

- Applying static grid spacing across assets

Tips for Better Results

- Use 200-bar lookbacks for stable percentile ranking

- Keep ATR smoothing at 14 periods

- Activate grids only above 70–80 ATR Percentile

- Deactivate below 30 ATR Percentile

- Monitor execution costs (fees, slippage)

- Combine with basic range or trend filters if needed

Tools or Resources

- Trading platforms supporting ATR indicators

- Quant frameworks for percentile ranking

- Backtesting engines for grid strategies

- Volatility regime dashboards

- Exchange APIs for automated execution

FAQ: Adaptive Grid Trading Strategy

What is ATR Percentile in trading?

ATR Percentile ranks current volatility relative to historical ATR values, expressing it on a 0–100 scale for normalization.

Why is ATR Percentile better than raw ATR?

Raw ATR varies widely across assets, while percentile ranking standardizes volatility signals for consistent decision-making.

When should grid trading be activated?

Only during high relative volatility regimes, typically above the 70–80 ATR Percentile.

Does this strategy work for trending markets?

It performs best in range-bound, high-volatility conditions and may struggle during strong persistent trends.

Can the same parameters be used for BTC, ETH, and SOL?

Yes. ATR Percentile normalization eliminates the need for asset-specific tuning.

What happens in low-volatility periods?

The strategy avoids or exits grids to prevent idle capital and unproductive trading.

Summary / Key Takeaways

- The Adaptive Grid Trading Strategy enhances grid trading using ATR Percentile-based volatility normalization

- It enables cross-asset deployment without manual optimization

- Grids activate only during favorable volatility regimes

- Capital efficiency and consistency improve significantly over static grids

- Best suited for systematic, multi-asset crypto portfolios