The Best Defensive Asset Class

Every market cycle eventually reminds investors of the same uncomfortable truth: stocks do not always go up. When drawdowns occur, the natural question becomes which assets actually protect capital when equities fall.

Defensive assets are supposed to do exactly that. They should either rise or at least remain stable during equity market downturns. But which asset class has historically done this best?

In this article, we review data and insights from a recent Allocate Smartly study, The Best Defensive Asset Class, which examines the historical performance of several defensive asset classes during periods (months) when US stocks declined. The results are more nuanced than many investors expect, unfortunately.

Related reading: –Best Defensive Investment Strategy

What makes an asset class defensive?

A defensive asset class is typically defined by three characteristics:

• low correlation to equities

• positive or stable returns during stock market declines

• ability to reduce portfolio drawdowns

Common candidates include government bonds, gold, commodities, and sometimes currencies such as the US dollar. However, labeling an asset as “defensive” does not guarantee it will always behave that way.

To evaluate this properly, we need long-term data.

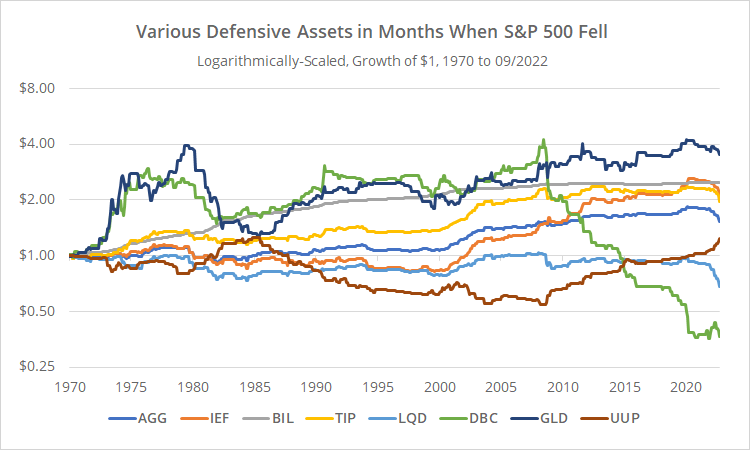

The dataset: how defensive assets behave when stocks fall

The analysis from Allocate Smartly uses monthly data from 1970 and focuses on months when the S&P 500 delivered negative returns.

Rather than analyzing full market cycles, this approach isolates the specific environments in which defensive assets are expected to perform: equity drawdowns.

The asset classes examined include:

• long-term US Treasuries

• intermediate-term US Treasuries

• short-term US Treasuries

• corporate bonds

• gold

• diversified commodities

• the US dollar

This provides a broad and realistic view of how different defensive assets behave under stress.

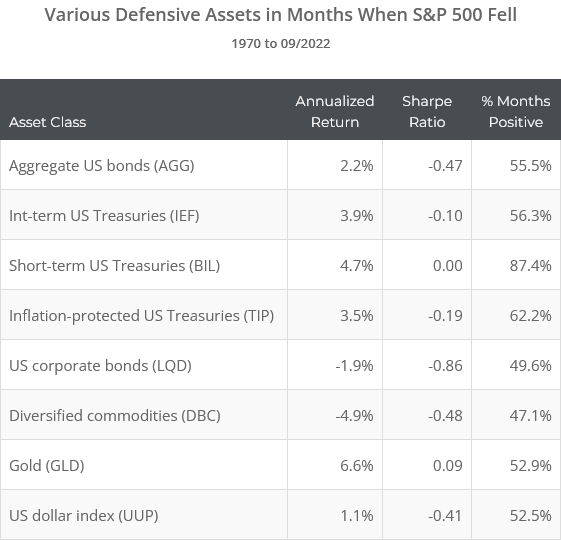

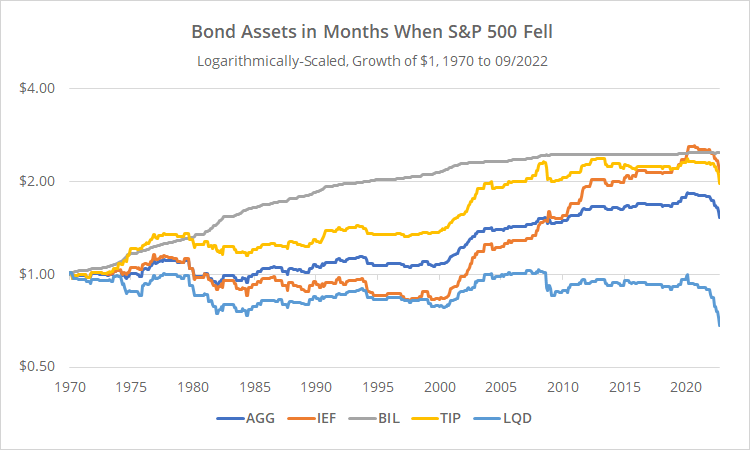

Bonds: reliable, but not risk-free

Government bonds are often considered the backbone of defensive investing, and history largely supports this view.

Long-duration US Treasuries performed well during many equity downturns and delivered positive returns in a majority of negative stock market months. However, they also experienced meaningful drawdowns during periods of rising interest rates, most notably in the 1970s and again recently.

Intermediate-term Treasuries showed more balanced behavior, while short-term Treasuries were the most stable but offered lower returns.

Corporate bonds, despite being labeled “bonds,” behaved much more like equities. During stock market declines, they often suffered alongside stocks due to credit risk.

Key takeaway: government bonds have historically been defensive, but interest-rate regimes matter.

Gold: strong long-term defense with uncomfortable drawdowns

Gold is often promoted as the ultimate defensive asset, and the long-term data gives it some credit.

Over the full sample, gold outperformed short-term Treasuries during months when stocks declined. That makes it the only asset class in the study to do so.

However, this outperformance came with significant volatility. Gold experienced long periods of underperformance and deep drawdowns, particularly outside of inflationary or crisis-driven environments.

Gold can be defensive, but it is not stable. Investors expecting smooth protection may be disappointed.

Commodities: defensive in theory, cyclical in practice

Diversified commodities showed defensive characteristics in earlier decades, especially during inflationary shocks. However, since the mid-2000s, commodities have increasingly behaved like risk assets.

During modern equity downturns, commodities have often declined alongside stocks, reducing their usefulness as a defensive allocation.

This highlights an important lesson: asset behavior can change over time.

The us dollar: inconsistent and unreliable as defense

The US dollar is sometimes viewed as a safe-haven asset, especially in global crises. Short-term studies may support this idea, but longer-term data tells a different story.

Across the full historical sample, the dollar’s performance during equity drawdowns was inconsistent and did not provide reliable defensive protection.

As a standalone defensive asset, the US dollar does not appear to be dependable.

Defensive assets in tactical asset allocation strategies

An interesting extension of the analysis looks at periods when tactical asset allocation strategies shifted into defensive assets.

During these periods, most defensive asset classes outperformed short-term Treasuries on average, with the notable exception of the US dollar.

This suggests that defensive assets may work best when combined with timing or regime-based signals, rather than as static long-term holdings.

So what is the best defensive asset class?

Unfortunately, there is no single asset class that consistently protects against all equity downturns.

• government bonds have been the most reliable overall, but are sensitive to interest-rate regimes

• gold has strong defensive properties but comes with high volatility

• commodities and currencies are far less reliable in modern markets

The broader lesson is that defense is context-dependent. Asset class behavior changes with inflation, monetary policy, and market structure. As is typical with markets, there are no “hard” rules. Everyting changes from time to time.

For investors, this argues for diversification, flexibility, and possibly systematic approaches rather than blind reliance on any single defensive asset.

Final thoughts

Defensive investing is not about eliminating risk, but about managing it intelligently. History shows that even traditional safe havens can fail under certain conditions.

Understanding how defensive assets behave across different environments is essential. Data-driven analysis, like the study discussed here, provides a much more realistic foundation than simple rules of thumb.

In markets, protection is never free — but informed choices can make drawdowns more manageable.