What Happens to Stocks When Bonds Decline – Historical Analysis (PDF)

When bonds go down and interest rates go up stocks perform poorly. A lower price for the bond means that the yield and interest rates go up, and future cash flows get discounted at a higher rate. When rates go up, it’s less attractive to own risky assets like stocks as it’s more attractive to own less risky assets. We backtest our hypothesis.

Jump to backtest.

The relationship between stocks and interest rates is at the center of financial theory. Why? Because the interest rates determine the value of stocks. High rates equal less appetite for owning risky assets, and investors will only own risky assets if they are compensated for taking this risk. What happens to stocks when bonds go down (what happens to stocks when interest rates go up)?

Key Takeaway

- Stocks typically perform poorly when bonds go down (i.e., when bond prices fall and interest rates rise), as higher rates make safer assets more appealing and discount future stock cash flows at a higher rate, reducing their present value.

- Bond prices and interest rates move inversely: when rates rise, existing bond prices fall because new bonds offer higher yields, making older ones less attractive.

- Stocks are riskier than bonds — in bankruptcy, bondholders get paid before stockholders, so bonds act as a safer haven during uncertainty or downturns.

- Historically, stocks and bonds often show a negative (inverse) correlation, providing diversification benefits in multi-asset portfolios; bonds tend to rise when stocks fall (e.g., during recessions), but this can flip to positive correlation during high inflation or rapid rate hikes.

- Backtests (e.g., using TLT for long-term Treasuries and SPY for S&P 500) confirm that periods when bonds decline (below moving averages) lead to lower average stock returns compared to random periods or when bonds are rising, aligning with financial theory that higher rates reduce appetite for risky assets like stocks. Past performance isn’t a guarantee of future results, and correlations can vary with economic conditions.

The inverse relationship between equity and bond returns has historically helped multi-asset portfolios weather various economic and market downturns. This dynamic is a key reason why diversification across asset classes is important for investors.

The inverse relationship between bonds and stocks

It’s crucial to understand the relationship between bonds and stocks. They both correlate to each other. When bonds go up in price, stocks also tend to go up. Higher bond prices mean the yield goes down, which is positive for stocks.

Opposite, when bond prices go down, meaning rates go up, it is bad for stocks.

Let’s give you a short primer on bonds:

A bond pays the same coupon during its life – until the bond matures. The coupon is paid annually to bondholders (for taking on the risk of owning it) until the bond’s maturity, when the principal amount is repaid to the investor. Maturity refers to the fixed period after which the bond issuer must repay the bond’s face value.

For example, a bond with a 5% coupon pays 5% until it matures. Let’s say 20 years. A one-billion-dollar bond with a 5% coupon pays 50 million annually to bondholders.

But during the bond’s life, interest rates fluctuate significantly. If the rates go down, the 5% loan is more attractive and thus investors bid the price of the bond up. Why? Because the price of the bond needs to go up to reflect the falling rates. The price of the one billion bond needs to go up 10% to reflect the change of the rates to 4.5% (this is just an example, in the real world a bond is influenced by a lot of factors).

When interest rates change, new bonds are issued with yields that match current rates, making existing bonds more or less attractive depending on whether their coupon is higher or lower than the new bonds. This means that stocks and rates have an inverse relationship.

Debt securities, including government and corporate bonds, are affected by Federal Reserve monetary policy decisions, which influence interest rates and, in turn, bond prices and yields.

Bonds are generally considered safer than stocks. Bonds tend to perform better during a recession than stocks, and during periods of economic downturns, investors often seek safety in high-quality fixed income investments, particularly U.S. Treasuries.

Bond market and fixed income

The bond market and fixed-income investments are foundational pillars of global financial markets, offering investors a way to balance risk and achieve relative portfolio stability. Unlike the stock market, which is known for its volatility and potential for rapid gains or losses, the bond market is generally seen as a safer haven, especially during periods of economic uncertainty.

At the heart of the bond market is the inverse relationship between bond prices and interest rates. When interest rates rise, the value of existing bonds tends to fall because newly issued bonds offer higher yields, making older bonds with lower interest payments less attractive.

Conversely, when interest rates fall, bond prices rise, and existing bonds with higher yields become more desirable. This dynamic is crucial for investors to understand, as it directly impacts the market value of their bond portfolio.

There are several types of bonds available to investors, including treasury bonds, government bonds, and corporate bonds. Treasury bonds, issued by the U.S. government, are often considered the benchmark for safety and a good hedge against market downturns.

Government bonds from other countries and corporate bonds issued by companies offer varying levels of risk and return, allowing investors to diversify their fixed income holdings according to their risk tolerance and investment objectives.

Bonds tend to perform well during market downturns or periods of high volatility, as investors seek the relative safety and fixed interest rate that bonds provide. However, when stock prices are rising and the economy is strong, investors may shift more money into equities, causing bond prices to fall.

The Federal Reserve’s monetary policy decisions, such as adjusting interest rates, play a significant role in shaping the bond market. When the Fed raises rates, yields rise on newly issued bonds, and the prices of older bonds typically decline, which can sometimes trigger a broader market crash if the adjustment is abrupt.

Asset allocation is key when investing in bonds and other asset classes. A well-constructed bond portfolio can help manage risk and provide steady interest income, even when other assets are underperforming. However, bonds are not without risk – rising interest rates, inflation, and changes in market conditions can all impact bond returns.

That’s why many investors tend to consult a financial advisor to help navigate the complexities of the bond market and ensure their investments align with their long-term goals.

In summary, understanding the bond market and fixed income sector is essential for anyone looking to build a resilient investment portfolio. By recognizing how bond prices react to changes in interest rates, and how different types of bonds fit into the broader landscape of financial markets, investors can make better decisions and better manage the risks and rewards of their investments.

Stocks are riskier than bonds

When a company goes bankrupt, what is left in the company is paid to the bond owners before anything is paid to equity holders. Thus, bonds are less risky than stocks. Bonds are often considered a safe haven during periods of stock market volatility and economic uncertainty, providing stability to portfolios when equities are under pressure.

When rates go up (bonds go down) it gets less attractive to own stocks. Stocks get bid down. When rates go down, it’s more attractive to own riskier assets like stocks, gold, and Bitcoin. When yields fall, investor preference may shift back to stocks, highlighting the dynamic interaction between yields and the stock and bond markets.

The bond and stock relationship is, of course, not constant. That is why both of them move up and down daily to adjust to new future expectations. A negative correlation between stocks and bonds means that when one asset’s returns decrease, the other’s tend to increase, which is important for diversification and risk management.

However, we believe it’s safe to anticipate that the correlation between bonds and stocks increases when inflation increases. The risk of persistently high inflation can undermine traditional multi-asset strategies and may push the correlation between stocks and bonds into positive territory, reducing diversification benefits.

Since the early 1980s, we have witnessed a 40-year bullish run with falling rates, in some countries even negative nominal rates, not to mention substantial negative real rates. Economic shocks, such as the Covid-19 pandemic or geopolitical crises, can also lead to positive correlations between stock and bond returns, as monetary policy responses may drive both asset classes in the same direction and move correlations into positive territory.

We hypothesize that a falling bond market is not good for stocks. Let’s backtest what happens to stocks when bonds go down:

We are long stocks (SPY) when bonds (TLT) are below the N-day moving average, and we sell when they’re above the N-day moving average.

For example, when TLT crosses below its 20-day moving average, we buy SPY at the close. When the close of TLT crosses above its 20-day moving average, we sell SPY at the close and are out of the market until TLT later crosses below its 20-day moving average.

What are SPY and TLT? SPY tracks the S&P 500, and TLT tracks US 20-year Treasury bonds. When TLT goes up in price, the interest rates go down, and vice versa.

Most investors benefit from a diversified portfolio that includes both stocks and bonds, as it typically helps meet long-term financial goals and reduces the risk of any single asset. Investing in stocks and bonds is essential for long-term investors seeking long-term returns. The lower the correlation between asset classes, the greater the diversification benefit.

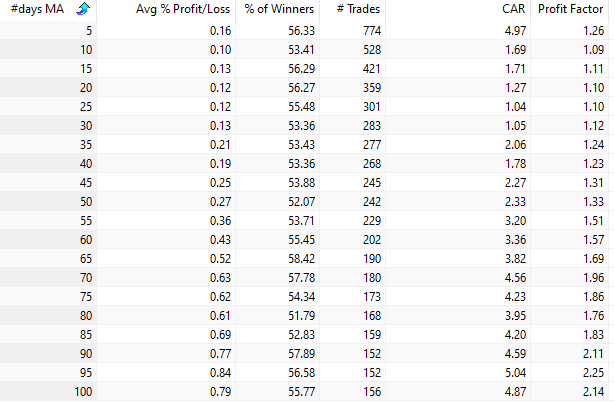

We backtest by doing an optimization where we test a wide range of moving averages from 5 days up to 100 with 5-day intervals (in total 20 backtests). The results look like this:

The first column shows the number of days in the moving average, and the following columns show the trading results for each number of days in the moving average. The important column is number 2, which shows the average gain per trade. The averages in column 2 are lower across all rows than on any random day.

Understanding the historical return patterns of equities and bonds can help manage risk in client portfolios. Global bonds can help reduce portfolio volatility, a key consideration in portfolio construction. Diversifying your investments can help reduce the risks associated with any one asset.

Backtest

Let’s look at a specific backtest: we chose the 15-day moving average. This is how the equity curve looks from 2003:

There are 421 trades, the average gain per trade is 0.13%, CAGR is 1.69%. Bonds have historically delivered smoother, more predictable returns compared to stocks during market downturns.

During the 2008 financial crisis, bonds outperformed stocks by a wide margin, providing relative safety to investors. In the 2020 market crash, U.S. government bonds performed well as investors sought stability amidst stock market declines, acting as a safe haven. Investors tend to seek safety in high-quality fixed income investments, particularly U.S. Treasuries, during economic downturns.

Investors often consider trading their portfolio during times of economic, financial, and political uncertainty.

Opposite, if we flip the buy and sell signals, we get much better results: What happens to stocks when bonds go up?

Inverse relationship between bond prices and interest rates – stock market performance – PDF

When bond prices fall and interest rates rise, stocks often underperform as higher rates make bonds more attractive and increase the discount on future earnings. Historical data using SPY and TLT shows equities yield lower returns during rising rates. Bonds remain a safer, diversifying asset, though high inflation can move both markets together. Understanding these dynamics and monetary policy is key for long-term portfolio strategy.

Conclusions

Our backtest shows what happens to stocks when bonds go down: they perform much worse than in any random period. This is consistent with financial theory and shows that it’s less desirable to own risky assets, such as stocks, when bonds decline.

However, it’s important to remember that the past performance of stocks and bonds does not guarantee similar future results. Investors should consider potential future results and evolving market conditions when making investment decisions. Stocks and bonds remain fundamental components of a long-term investment strategy, and understanding their relationship is crucial for effective portfolio construction.

FAQ:

What happens to stocks when bond prices fall?

When bond prices fall, interest rates rise. Higher interest rates make safer fixed-income assets (like bonds) more attractive compared to risky assets like stocks. In addition, future cash flows from stocks are discounted at a higher rate, which reduces their present value. As a result, stocks typically perform poorly during periods when bonds decline. Historical data and backtests confirm that stock returns are meaningfully lower in these environments compared to random periods or when bonds are rising.

Why are stocks considered riskier than bonds?

When bond prices rise, it usually implies a decrease in interest rates. In this scenario, bond yields become more attractive than stock yields. In the event of bankruptcy, bondholders are paid before equity holders. Thus, bonds are considered less risky than stocks.

What is the correlation between bonds and stocks?

The correlation between bonds and stocks is a crucial aspect of financial markets. Generally, these two asset classes exhibit an inverse relationship, meaning their prices often move in opposite directions. Understanding this correlation is essential for investors and traders in managing portfolios and making informed decisions.

How do bonds and stocks adjust to new future expectations?

A falling bond market is hypothesized to be unfavorable for stocks. Both bonds and stocks adjust daily to new expectations, leading to continuous movement. The correlation between them may increase as inflation rises. It’s important to note that while this inverse correlation is a general trend, market dynamics can be influenced by various factors, including economic conditions, central bank policies, geopolitical events, and investor sentiment.

Can investors invest directly in unmanaged indices like the S&P 500 or bond indices?

No, most investors cannot invest directly in unmanaged indices such as the S&P 500 or major bond indices. Instead, to gain exposure to these indices, investors typically use investment vehicles like ETFs or mutual funds. These funds are designed to track the index’s performance but may incur costs and tracking differences relative to the index itself.

Why do bond prices and interest rates move in opposite directions?

Bond prices and yields (interest rates) have an inverse relationship. When market interest rates rise, newly issued bonds offer higher yields, making existing bonds with lower fixed coupons less attractive. To compete, the price of those older bonds must fall so their effective yield matches the new higher market rates. The opposite happens when rates fall: existing bonds become more valuable, and their prices rise.