The Rise of Sports Data Arbitrage: How Algorithmic Traders are Capitalizing on Real-Time Athletic Metrics

Image source: Pexels

Why are institutional investors suddenly treating player health and game momentum like blue-chip stocks? In 2026, the answer lies in the data. Sports have evolved from a weekend pastime into a high-fidelity data stream, generating millions of metrics per second. For the modern trader, these are not just highlights; they are inefficiencies waiting to be exploited.

By applying the same mechanical rules found in a Trend Following Strategy, algorithmic traders are now capturing alpha in the “sports ecosystem era,” where real-time athletic performance is the new asset class.

The Quantified Approach to Athletic Performance

Traditional sports analysis often relies on “gut feeling” or historical averages. However, much like the transition from manual floor trading to algorithmic execution, sports investing has moved toward a quantified model. Analysts now use machine learning to process biomechanics and fatigue levels, effectively creating a “moving average” for player output.

When a star player’s efficiency drops below a certain standard deviation, the market reacts. This shift mirrors how a trader might use a Stochastic RSI to identify overbought or oversold conditions, applying rigorous backtesting to player “value” rather than ticker symbols.

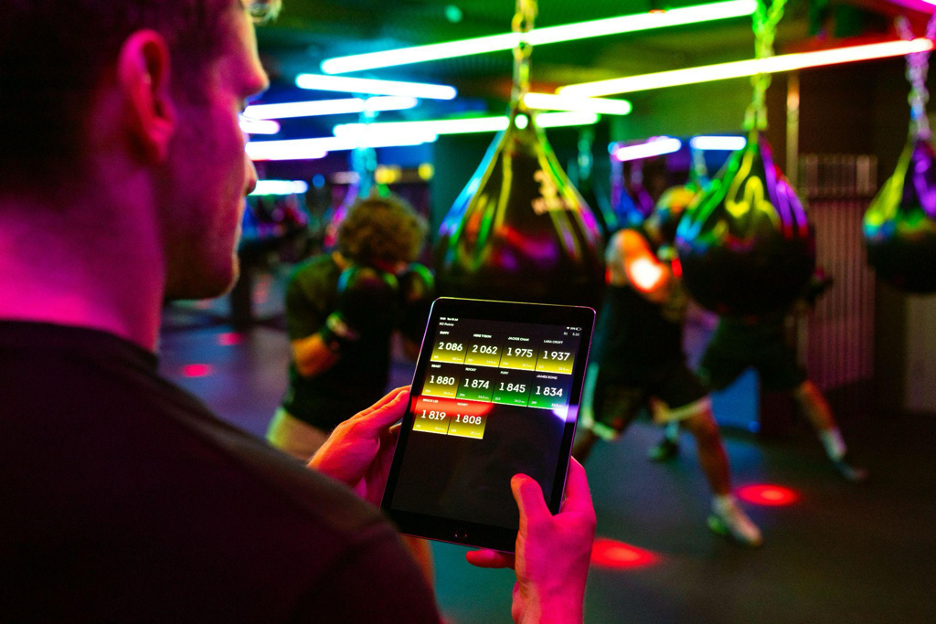

Scaling Through Integrated Digital Infrastructure

The success of sports data arbitrage depends on the robustness of the underlying technology. For these strategies to work, data must be processed in sub-100 ms windows to beat valuation changes. This level of technical sophistication is now a cross-industry standard; it is mirrored in the high-volume digital environments of global platforms like Gaming Club, the low-latency execution engines of Citadel Securities, and the massive real-time streaming infrastructure of Twitch.

Just as these systems ensure near-instant synchronization for millions of concurrent users, the sports arbitrageur relies on similar ‘edge computing’ to ensure their player metrics reflect the most recent on-field action.

Backtesting the “Predictive League Office”

One of the most significant shifts in 2026 is the rise of the “Predictive League Office.” According to recent industry reports from N3XT Sports, organizations that centralize their data see a 15–30% increase in audience engagement and operational ROI. For a trader, this centralized data is a goldmine for backtesting.

By running simulations on how specific in-game events affect a team’s long-term market valuation, investors can build systems that operate with high predictive accuracy. This is the same logic used to evaluate the 10 Best Swing Trading Strategies, shifting the focus from individual game outcomes to long-term statistical trends.

Managing Risk in a Volatile Data Market

Volatility is inherent in both the stock market and professional sports. An injury or a sudden weather shift can derail a season, just as a geopolitical event can shake the markets. To mitigate this, traders are adopting Position Sizing Strategy Types specifically tailored for athletic data.

Instead of betting on a single outcome, they diversify across a portfolio of metrics—such as player speed, ball velocity, and defensive pressure. This “system over spectacle” approach ensures that even if one athlete underperforms, the overall mathematical model remains robust.

The Future of Data-Native Investing

As we move further into the year, the “Ecosystem Era” of sports will only accelerate. The organizations that treat data as a strategic pillar rather than a byproduct are the ones defining how sports are governed and commercialized.

For the individual trader, the lesson is clear: the same discipline, backtesting, and mechanical execution that work for a Breakout Trading Strategy are now the keys to unlocking value in the world of professional sports metrics.