Global Equities Momentum Strategy

A compelling approach to tactical asset allocation is the global equities momentum strategy, originally called “Enhanced” Global Growth Cycle (GGC) strategy, developed by Grzegorz Link, and referred to by Allocate Smartly.

This strategy builds on the original GGC by combining the OECD Composite Leading Indicator (CLI) with momentum filters to determine not only when to take risks, but also which assets to hold.

Related reading: –Quantified investment strategies

Trading Rules

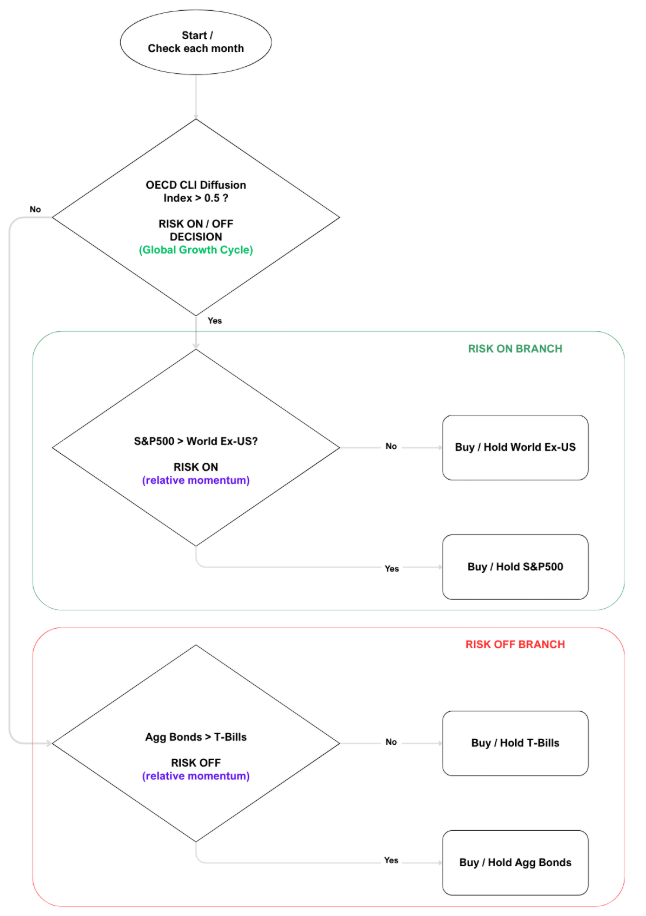

The core of the strategy relies on a Diffusion Index (based on CLI data) calculated at the end of each month. Because there is a reporting delay, the strategy uses CLI data from the previous month-end (a 1-month lag). The Diffusion Index measures the percentage of countries whose CLI value rose month-over-month.

Grzegorz Link made a helpful flow chart laying out the trading rules:

- Risk On: If the Diffusion Index is greater than 50%, the strategy moves into risk assets. The Diffusion Index measures the % of countries whose CLI value rose month-over-month.

- Risk Off: If the index is 50% or lower, the strategy shifts to defensive positions.

This is not all. Unlike the original version by Grzegorz Link, the “Enhanced” GGC by Allocate Smartly uses 12-month momentum to refine its holdings. Once the risk signal is determined, the strategy follows these rules:

- During Risk-On Periods: It compares the 12-month returns of US stocks (SPY) against international stocks (IEFA). It allocates 100% of the portfolio to whichever has the higher momentum.

- During Risk-Off Periods: It compares US aggregate bonds (AGG) against short-term US Treasuries (BIL). If bonds outperform Treasuries, it holds AGG; otherwise, it moves to cash.

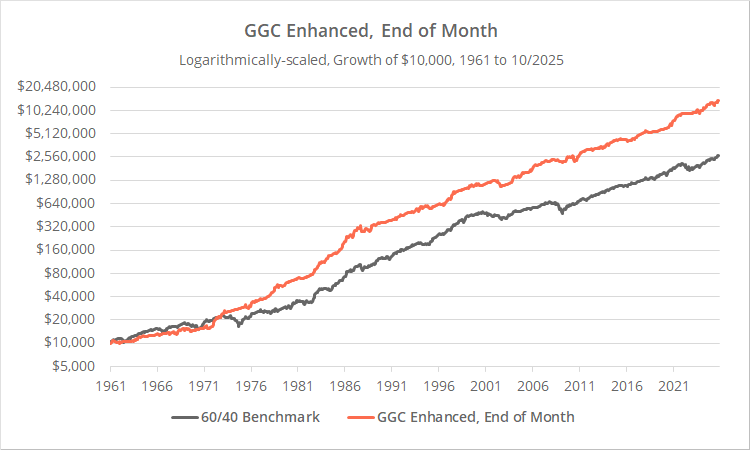

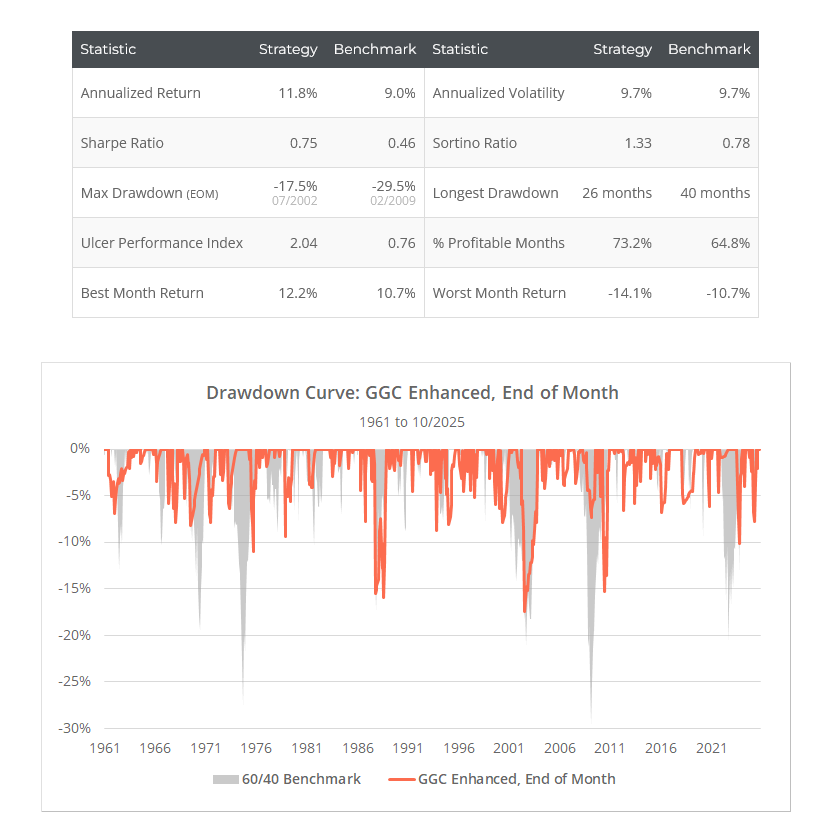

Results And Performance

The global equities momentum strategy has performed well:

Timing Your Trades: Monthly vs. Mid-Month

While the standard strategy executes at the end of the month, the sources also tracked a mid-month version. Because OECD CLI data is typically released in the first two weeks of a month, trading on the 15th calendar day allows the strategy to react more quickly to new information.

Although mid-month trading outperformed significantly in the 1980s, the two versions have tracked each other closely in more recent decades.

Which Version Should You Choose?

The best version of the GGC strategy depends on your overall portfolio goals:

- For a Standalone Strategy: The global equities momentum strategy is often preferred because it incorporates momentum, a fundamental market force that has historically driven long-term performance.

- For a Diversified Portfolio: The original GGC may be superior. Because many tactical strategies already use momentum, the original GGC provides a “purer” economic signal with lower correlation to other assets, helping to smooth out overall performance.

Despite the complexity of vintaging and data revisions, the Enhanced GGC has proven resilient on “unseen” data, making it a robust option for investors looking to time the market using macroeconomic indicators