ETF Rotation Strategy for High Returns (Backtested)

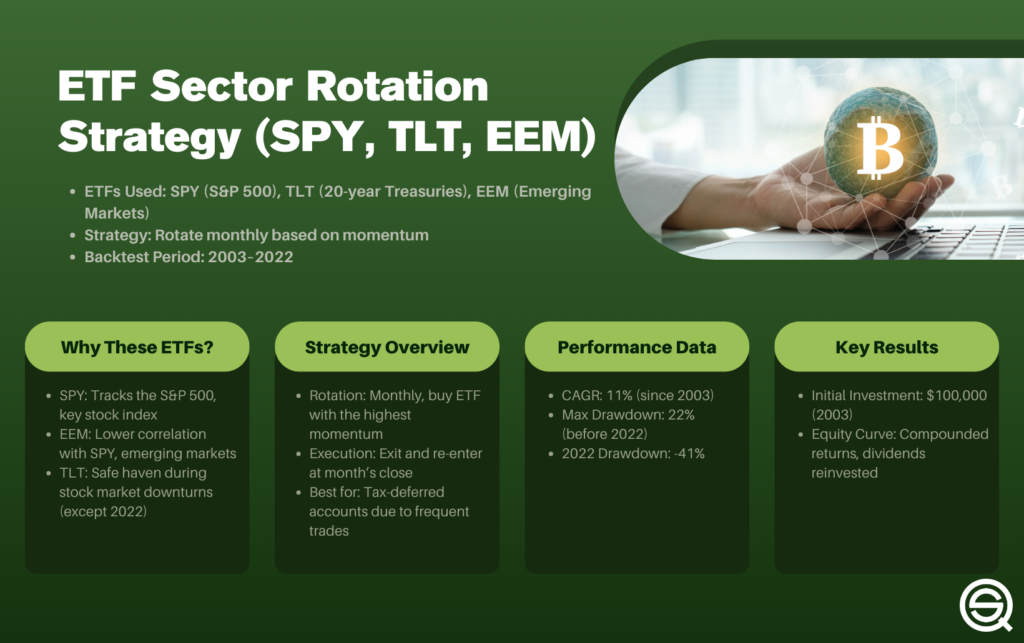

This article presents an ETF rotation strategy. Sector rotation is popular, and this is not without merit. The idea is to be in the sector that shows the best recent momentum. Today we present an ETF momentum rotation trading strategy based on monthly data in EEM, SPY, and TLT.

ETF sector rotation strategies can offer diversification across industries and asset classes, helping investors manage risk and optimize returns. As a type of fund, ETFs allow investors to access a wide range of assets, providing flexibility and liquidity. By investing in several different sectors at the same time, investors can create a more diversified portfolio and reduce exposure to individual sector risks.

In this short article, we give an example of a very easy and simple ETF rotation strategy among SPY (S&P 500), TLT (Treasury bonds), and EEM (MSCI Emerging Markets) that has worked pretty well over the last two decades. It has beaten “buy and hold” with lower drawdowns. That was until 2022, which was a very bad year for the strategy.

Table of contents:

SPY is an ETF that tracks the S&P 500, TLT tracks the 20-year Treasury bonds, while EEM tracks the MSCI Emerging Markets Index. ETFs allow investors to take advantage of investment opportunities in many industry groups throughout the world.

Why did we choose these three ETFs?

SPY was chosen because it’s the most important stock index on the planet. The S&P 500 is, by far, the most followed stock index on the planet.

The EEM was chosen because it correlates less with the SPY. Emerging markets often behave differently than the stock markets of the Western world.

Lastly, TLT was included because it’s often a “safe haven”. When the stock markets turn ugly, many seek refuge in the safe harbor of US long-term Treasury bonds. Unfortunately, this didn’t happen when the markets turned ugly in 2022.

ETFs are highly liquid funds, making it easy to adjust exposure to different sectors or assets as market conditions change.

EEM and TLT provide exposure to different sectors and geographic regions, helping diversify across various industries and asset classes. ETFs have low expense ratios compared to actively managed mutual funds, making them a cost-effective way to gain exposure to various sectors and industries.

The performance of different sectors can be influenced by the stage of the business cycle, calendar effects, or geographic trends.

That’s the theory. Does it hold up in practice?

Our sector rotation strategy in TLT, SPY, and EEM

Yes, the theory held up pretty well in the backtest we did over two decades. The principal goal of the sector rotation model is to help investors reallocate their portfolio to the best-performing sectors each month, seeking higher returns by actively allocating to the strongest market sectors. This model uses a rules-based approach to analyze market data and identify top-performing sectors, aiming to optimize future performance while managing additional risk.

This is what we did (trading rules and settings):

We entered and exited sector ETFs monthly based on momentum signals. The model continuously reallocates capital to the strongest-performing sectors, allowing for higher growth potential.

Drawdowns were generally lower than the market, and the strategy outperformed the S&P 500 over the test period. Using sector-specific ETFs instead of individual stocks reduces the additional risk of one company’s failure severely impacting the portfolio. Investors can create a more diversified portfolio by investing in several different sectors at the same time, weighted according to future performance expectations.

A 2023 study found that sector rotation strategies showed modest outperformance, which diminishes after accounting for transaction costs. The effectiveness of sector rotation has been disputed, as it requires correctly anticipating market downturns and sector performance, and mistiming can lead to selling winners too early or buying into hot sectors at their peak. Accurately predicting market turns is difficult, as rotation strategies often rely on hindsight, leading to poor timing.

Understanding the Economic Cycle

A solid grasp of the economic cycle is fundamental for investors looking to maximize the effectiveness of a sector rotation strategy. The economic cycle consists of four main stages: expansion, peak, contraction, and trough. Each stage influences the performance of different sectors within the market, making it crucial for investors to recognize where the economy stands.

During the expansion phase, economic growth accelerates, consumer confidence rises, and businesses invest in innovation. In this environment, sectors such as technology and consumer discretionary often outperform, as consumers and companies are more willing to spend on new products and services. As the cycle approaches its peak, growth slows, and investors may begin to shift capital toward sectors that are less sensitive to economic fluctuations.

When the economy enters a contraction or recession, risk increases and market volatility tends to rise. Defensive sectors like consumer staples and health care typically perform better during these periods, as demand for essential goods and services remains steady regardless of economic conditions. By rotating investments into these defensive sectors, investors can manage risk and protect their portfolios from significant losses.

A well-executed rotation strategy leverages these cyclical trends, allocating capital to sectors that are expected to outperform in the current phase of the economic cycle. This proactive approach not only helps manage risk but can also enhance returns over time. Understanding how sectors tend to behave in different economic environments empowers investors to make informed decisions and optimize their investment performance.

Trading Rules

At the end of each month, we rank the ETFs. We go long (buy) the one with the best performance over the last month (in %).

This is all there is to it. It can hardly get any simpler than that.

Obviously, this strategy is best performed in a tax-deferred account because of the frequent rotation among the ETFs.

Without slippage and taxes, the equity curves look like this (from 2006 until today):

Monthly Momentum Strategy EEM SPY TLT

The equity curve shows compounded returns and dividends reinvested.

If you invested 100,000 on the first day of 2003, the strategy has compounded pretty well until it hit a wall in 2022:

The entry and exit are done at the close of each month and commissions and slippage are not included. The CAGR since inception is 9.4% despite the setbacks lately. Before 2022 max drawdown was 22%, but the portfolio fell 44% from the peak in 2022 (!).

However, if we change the trading rules and base the strategy on the best performance over the last 3 months, the results improve. We still rank the ETFs every month, but the ranking is based on the performance over the last 3 months (not one month).

The annual returns go up to 11.5%, while the max drawdown is reduced to 32%.

Code for Rotation strategies

If you want the code for the strategy, you find it among our memberships.

Evaluating Performance against the S&P 500

When implementing a sector rotation strategy, it’s essential to evaluate its performance against a reliable benchmark like the S&P 500. The S&P 500 serves as a standard for measuring the overall health and trends of the US stock market, making it a valuable point of comparison for any rotation strategy.

A sector rotation strategy that consistently outperforms the S&P 500 can offer investors a significant advantage, especially in changing market conditions. However, it’s important to look beyond headline returns. Factors such as transaction costs, tax implications, and the ability to adapt to dynamic market trends all play a role in determining long term performance. For example, frequent trading between sector ETFs can increase transaction costs and potentially impact after-tax returns.

To maximize the benefits of a rotation strategy, investors should regularly monitor performance, adjust allocations in response to evolving economic and market trends, and ensure the strategy remains aligned with their risk tolerance and investment objectives.

A dynamic sector rotation approach, one that responds to changing market conditions, can help investors stay ahead of the curve and achieve their long-term goals. By carefully considering costs and maintaining a disciplined evaluation process, investors can better position themselves to outperform the S&P 500 and capture opportunities as they arise.

Managing Risks and Benefits of Sector Rotation Strategies

Sector rotation strategies offer a range of benefits, including the potential for enhanced returns, improved diversification, and more effective risk management. By shifting investments among sectors based on market trends and economic expectations, investors can capitalize on opportunities and potentially outperform the broader market.

However, these strategies also come with certain risks. Frequent trading can lead to higher transaction costs, which may erode gains over time. There’s also the risk of allocating capital to certain sectors that may not perform as expected, especially if market conditions change rapidly or if the strategy is not implemented with discipline. Additionally, relying solely on past performance does not guarantee future results, and investors must be prepared for periods of underperformance.

To manage these risks, it’s important for investors to clearly define their investment objectives, assess their risk tolerance, and consider their time horizon before adopting a sector rotation strategy. Conducting thorough research, reviewing the strategy’s historical performance, and understanding all associated costs are essential steps. Working with a financial advisor or using a rules-based, systematic approach can help minimize emotional decision-making and ensure the strategy is executed consistently.

By weighing the potential benefits against the risks and maintaining a disciplined approach, investors can use sector rotation strategies to diversify their portfolios, manage risk, and pursue long-term financial goals with greater confidence.

ETF rotation strategy – conclusion:

The ETF rotation strategy we presented in this article has performed reasonably well, but not in the last 5-6 years.

FAQ:

– What is the ETF rotation strategy, and how does it differ from traditional sector rotation strategies?

The ETF rotation strategy involves monthly rotation among SPY (S&P 500), TLT (Treasury bonds), and EEM (MSCI Emerging Markets) based on their recent performance. It differs from traditional sector rotation by focusing on specific ETFs rather than broader market sectors.

Investors typically define a “universe” of ETFs to monitor, such as the 11 major S&P 500 sectors or various asset classes, and the strategy focuses on these selected ETFs to optimize opportunities.

– How does the ETF rotation strategy work in practice?

The strategy involves ranking SPY, EEM, and TLT based on their previous month’s performance and going long on the best-performing ETF. This position is held for one month, and the process is repeated. Investment managers may employ specialized rotation techniques such as sector rotation, momentum-based rotation, and geographic rotation. It’s a simple strategy that requires minimal monthly effort.

– What are the key considerations for investors interested in the ETF rotation strategy?

Investors should consider the historical performance, drawdowns, and recent challenges faced by the strategy, such as the impact on CAGR and drawdown after 2022. Additionally, understanding the strategy’s simplicity and ease of implementation is crucial before making investment decisions. Tactical ETFs allow quick shifts to new market leaders, enabling investors to adapt to changing economic conditions.