Random Walk Theory Trading Strategy: Random Entries Beating the Market? (Backtest)

Random Walk Theory Trading Strategy means stock prices move randomly and can’t be predicted — like flipping a coin. Popularized by Burton Malkiel in A Random Walk Down Wall Street, the idea suggests that trying to time the market is mostly guesswork.

Because short-term moves are unpredictable, some traders use random entries instead of hunting for perfect setups. We even backtested a random-entry approach to see how it performs in real markets. The logic is simple: timing matters less than diversification and risk control. By spreading investments widely or owning an index like the S&P 500, investors can still benefit from the market’s long-term upward drift despite short-term randomness.Jump to backtest.

The random walk theory was popularized by economist Burton Malkiel in his 1973 book, A Random Walk Down Wall Street. The theory has historical roots traced back to early 20th-century mathematicians, such as Louis Bachelier, and is a foundational concept in financial economics. According to Malkiel, the market moves randomly and its direction cannot be predicted with fundamental or technical analyses. But is the market truly random, and what is a random walk trading strategy?

Key Takeaways

- Random Walk Trading Strategy: A method of investing that relies on random entries and exits rather than market timing or analysis. It assumes stock prices are unpredictable, so the best approach is to own a widely diversified portfolio (like an index fund) to capture the market’s long-term upward trend.

- The 50/50 Probability Rule: Random Walk Theory assumes stock prices are completely unpredictable, meaning there is an equal chance a price will rise or fall at any given time, making traditional “market timing” futile.

- Rejection of Analysis: The strategy suggests that because price movements are independent of the past, both technical analysis (charts) and fundamental analysis (earnings) provide no consistent advantage for forecasting.

- The Power of Passive Indexing: Since individual winners are impossible to pick reliably, the best application of this theory is broad diversification through index funds (like the S&P 500) to capture long-term market growth while minimizing risk.

- The “Upward Drift” Edge: Backtesting proves that random entries actually work well in the stock market (S&P 500) because of a natural upward bias driven by inflation and productivity—a “tailwind” not found in all assets like Gold.

- Luck vs. Skill: Historical experiments (like the WSJ Dartboard Contest) show that professional managers rarely outperform random stock selection once fees are considered, supporting a “buy and hold” approach for the average investor.

In this post, we take a look at the random walk concept and how to apply it to trading. At the end of the article, we make a backtest of the strategy.

(We recommend Burton Malkiel’s book. It’s a good book about investing and lets you understand more how markets work.)

What does the random walk trading strategy mean?

Random walk theory is a financial market model that assumes that stock prices move in a completely unpredictable way. In other words, the future price of each stock is independent of its own historical and current price movement and market reactions to news about the stock are random. This hypothesis assumes that all forms of stock analysis — technical, fundamental, and sentiment analyses — are unreliable and pointless, as proponents believe that neither fundamental nor technical analysis can effectively predict future movements due to market efficiency.

With no degree of predictability in the movement of stock prices, it means that stock prices are random. According to the random walk theory, past events and historical price movements do not provide any reliable information for predicting future movements. Thus using historical prices to forecast future price movements is futile, as changes in stock prices have the same distribution and are independent of each other.

A stock that is priced at $50 today can sell for $70 or $30 tomorrow, and there is no way of knowing which way it would go. According to this theory, the stock price movement is like the toss of a coin — it could come up head or tail, and you cannot know which side it would be.

Since the past movement or trend of a stock price or market cannot be used to predict its future movement, it is pointless trying to analyze how the price might move in the future. If stocks take a random and unpredictable path, then all methods of predicting stock prices are futile in the long run. So, one may be better off making random entries and exits, and this is the random walk trading strategy.

The random walk trading strategy assumes there is a 50% probability that the stock price will rise then there is a 50% probability that the stock price will fall. And as such, it is difficult to beat the market. Even if that is true — that stocks have a 50% chance of rising or falling, a study of the broad market index, such as the S&P 500 index, shows that the market has a tendency to go up over the long run, in spite of the short-term fluctuations. We have made a separate article that covers the “overnight trading edge“.

If that is the case, a random walk trading strategy that only buys an index ETF might present a good way to make money off the market.

How a random walk trading strategy works

The application of the random walk theory in trading is that you don’t put all your eggs in one basket, as at every point in time, the stock has a 50% chance of rising or falling. If you risk all of your hard-earned cash on that single stock, if the stock’s price falls, you lose money, and if it rises, you gain money.

Since the movement is random, you don’t know when it’s going to rise or fall, and your ability to gain or lose is tied to that one stock. Attempting to outperform the market typically requires taking on additional risk, which is not recommended by the random walk theory.

The theory advocates for a long-term investment strategy, emphasizing a buy-and-hold approach and focusing on long-term growth rather than trying to time the market or pick individual stocks.

Diversification is key, and index investing is a practical way to implement a passive investment approach. Random walk theory has led to the rise of passive investment strategies, such as index funds, which aim to replicate overall market performance without trying to outperform it through active management.

Backtested trading strategies

With the random walk trading strategy, you spread out your risk in a bunch of different stocks instead of putting it all into a single stock. So, when one stock underperforms, another might outperform and offset the loss from the underperformer. This minimizes your chances of losing everything and may also lead to more returns in the long run.

The key takeaway from the random walk trading strategy is to stop trying to time the market and instead, use the powers of risk diversification to our advantage. Even professional money managers often fail to consistently outperform the overall market, which is why passive investing strategies that track the market have become increasingly popular.

VIDEO Random Walk Theory with random trading entries

Random Entry Trading Works. Can a strategy with zero indicators actually beat the market?

In the video below, I backtest the Random Walk Theory to see how a completely random approach performs. By stripping away the noise and using just 12 trades a year with a four-day hold, the results are a humble reminder that trade management often outweighs the “perfect” entry.

Efficient market hypothesis – a random walk in stock prices

You may be wondering how the random walk theory relates to the efficient market hypothesis. Let’s find out.

According to the random walk theory, which is grounded in probability theory, share price movements are caused by random and unpredictable events. Proponents of the random walk theory argue that stock prices move independently of past data, making accurate forecasting impossible and dismissing the existence of patterns or inefficiencies that could be exploited by skilled investors.

For instance, how the market reacts to unexpected events depends on how investors perceive the event, which is random and unpredictable too. As a result, trying to analyze and time the market is a futile adventure.

The efficient market hypothesis (EMH), on the other hand, is built on the concept of market efficiency. It theorizes that asset prices fully reflect all information available in the market, so it is not possible to find any edge in the market, let alone beat the market. The EMH is classified into three distinct tiers:

- Weak Form EMH: In this version, all past information, such as historical trading prices and data regarding volume, is reflected in the market prices. So, there is no need to perform technical analysis to find an edge.

- Semi-Strong EMH: In this version, all public information, including news and company earnings, available to all market participants is reflected in the current market prices.

- Strong Form EMH: In this version, all public and private information, even the knowledge of insiders, is reflected in the current market prices.

Obviously, the random walk and efficient market theories are based upon different assumptions — the former assumes that the market is random, while the latter assumes that the market is efficient. However, both hypotheses arrive at virtually the same inference, which is that it is nearly impossible to consistently outperform the market. They both support passive investing in broad market index funds over active trading strategies.

Despite their similar conclusions, both theories diverge in so many ways. Here is a table that shows the differences:

| Efficient Market Hypothesis | Random Walk Hypothesis |

|---|---|

| The market is assumed to be efficient, so market prices can neither be undervalued nor overvalued. | The market is irrational and walks randomly in any direction it pleases at any point in time — doesn’t care whether you adjudge it overvalued or undervalued. |

| The theory assumes that the market corrects itself instantaneously once new information is made public. | Movements are random, as participants’ reactions to any new information are random. |

The problem with both theories is that they fundamentally contradict each other. If the market were hypothetically efficient, as proposed under EMH, then asset prices are rational, so market fluctuations are not necessarily random as claimed by the random walk theory.

On the other hand, if the random walk theory were valid, it implies that the market is irrational, which negates the proposal of the efficient market hypothesis.

Another issue with the EMH is the assumption that the market corrects itself instantaneously once new information is made public. But many times, share prices take time before stabilizing, especially for thinly traded securities. Whichever way, one cannot deny the influence of unexpected events. There are recognizable trends and behavioral patterns among market participants, such as momentum and overreaction, which can directly impact share prices.

Critics argue that random walk theory oversimplifies the complexities of financial markets and dismisses the possibility of patterns or inefficiencies that skilled investors could exploit. The theory also assumes that all investors have the same information, which is often not the case in reality.

Some investors believe that certain events, like market bubbles or crashes, show that price movements can follow predictable patterns, challenging the theory’s assumptions. The non random walk perspective suggests that technical analysis and trend-based predictions can sometimes identify opportunities, and critics often point to successful investors like Warren Buffett as evidence that it is possible to outperform the market through skillful analysis.

Both the Random Walk Theory and EMH are based on strict assumptions that are unlikely to be realistic. And, as proven by many investors and traders, some go on to make spectacular track records over many decades. One of them is Warren Buffett. This is what he once said about the EMH:

I think it’s fascinating how the ruling orthodoxy can cause a lot of people to think the earth is flat. Investing in a market where people believe in efficiency is like playing bridge with someone who’s been told it doesn’t do any good to look at the cards.

What are the rules for the random walk trading strategy?

The key to the random walk trading strategy is diversification, which allows you to take advantage of the supposed randomness in the market. But how do you build a diversified portfolio of stocks? There are basically two ways of doing that:

- Build a stock portfolio on your own: You can build a diversified portfolio of stocks by investing in stocks in different industries and sectors. The idea is to buy stocks that are not correlated so that when some are not performing well, others that are performing well would offset the losses. You should have a portfolio of more than 20 stocks in different industries and market sectors.

- Index investing through a broad market index ETF: An easier way to achieve diversification is to use index investing by putting your money into a broad market index fund. Index investing aims to replicate the performance of the overall market, rather than trying to pick individual winners. A broad market index tracks the entire market, unlike a sector index that tracks only a market sector. A broad market index fund takes your money and spreads it out across a shared reasonable portfolio of the overall market, so your money is well diversified. With a broad market index fund, to lose all of your money, the entire market would have to crash. And, realistically, the likelihood of the overall market crashing is much lower than the risk of an individual stock crashing. Some of the popular index funds you can trade include:

- iShares Core S&P 500 ETF (IVV)

- Invesco QQQ ETF (QQQ)

- Fidelity ZERO Large Cap Index (FNILX)

- SPDR S&P 500 ETF Trust (SPY)

Pros and cons of the random walk strategy

There are many merits and demerits of the random walk investment strategy. The merits include the following:

- Passive investing: The random walk strategy recommends passive investing, which does not require you to try to time the market or pick individual stocks you think may become winners. So, you remove the possibility of getting it wrong and simply move with the market. You invest and forget about it. Women have proven to be better investors than men, and the most likely reason is that they are not trying to be smart. They invest and forget about it.

- Diversification: The random walk strategy emphasizes diversification as a way to reduce the risk of individual stocks performing poorly after buying them.

- Long term investment strategy: The random walk theory advocates for a long term investment strategy, focusing on buy-and-hold, diversified portfolios, and patience. Rather than attempting to predict short-term market movements, investors are encouraged to adopt a long-term approach for better results.

The demerits of this strategy include the following:

- Systemic risk: Neither building a stock portfolio nor investing in an index fund removes systemic risk. The entire market can crash and you lose money. No amount of stock portfolio diversification can remove that risk. However, the best way to hedge against systematic risk is to have uncorrelated assets.

- Unlikely to become rich, or at least require a lot of time: It is difficult to make a lot of money investing in an index fund unless you already have a lot of money. It takes decades to save and invest to make a decent nest egg. Many are dreaming of becoming a F.I.R.E.:

- What is FIRE?

- Additional risk: Achieving market outperformance typically requires taking on additional risk, which may not align with the principles of the random walk theory. The theory suggests that trying to beat the market by accepting higher levels of risk is not a guaranteed or advisable strategy.

Charlie Munger, Warren Buffett’s friend and partner, once said that the best edge in the market he and Warren have is that they are trying to get rich slowly, not quickly.

Where does it originate from? (History)

The random walk theory was first coined by French mathematician Louise Bachelier, who believed that share price movements were just like the steps taken by a drunk — unpredictable! But it was economist Burton Malkiel who made the theory popular through his book, A Random Walk Down Wall Street. Both Bachelier and Malkiel contributed significantly to the field of financial economics, which studies the random character of stock prices and the concept of market efficiency.

Published in 1973, the book explains that stock prices take a completely random path. As such, the probability of a share price increase at any given time is exactly the same as the probability that it will decrease. In fact, Malkiel argues that a blindfolded monkey could randomly select a portfolio of stocks that would do just as well as a portfolio carefully selected by professionals.

The random walk hypothesis is related to the efficient market hypothesis, an earlier theory posed by University of Chicago professor William Sharp. Malkiel’s book is frequently cited by those in favor of the efficient-market hypothesis, as both theories agree it is impossible to outperform the market. Whether you agree or disagree with the theory, we strongly recommend reading the book.

However, while the EMH argues that the market is efficient and all of the available information will already be priced into the stock’s price, random walk implies that the market is irrational.

Sharp and Malkiel tried to show that it is impossible to exploit mispriced stocks consistently because price movements are mostly random and driven by unforeseen events. They are of the opinion that, due to the short-term randomness of returns, investors would be better off investing in a passively managed, well-diversified fund. And the evidence is pretty strong against the small retail investor: they, as a group, underperform massively, but also because they do cognitive mistakes (buy tops and sell into panics).

Random walk strategy example

The most well-known practical example of random walk theory was the experiment performed in 1988 by the Wall Street Journal. The Journal sought to test Malkiel’s theory by creating the annual Wall Street Journal Dartboard Contest, specifically designed to test Malkiel’s theory. In this contest, money managers (professional investors) were pitted against darts for stock-picking supremacy. Wall Street Journal staff members played the role of the dart-throwing monkeys.

The results showed that money managers won 87 contests, while the dart throwers won 55 contests. However, money managers only beat the Dow Jones Industrial Average (DJIA) in 76 contests out of 140, which is not a statistically significant difference. Reacting to the result, Malkiel suggested that the experts’ picks could have benefited from the publicity jump in the price of a stock that tends to occur when stock experts make a recommendation.

Since money managers could only beat the market half the time, when you consider management fees, it becomes clear that investors would be better off investing in a passive fund that charges far lower management fees. This underperformance by money managers has contributed to the rise of passive index investing and its increasing popularity among investors.

Random Walks and Market Volatility

The random walk theory suggests that stock prices are subject to unpredictable and random events, which naturally leads to market volatility. In financial markets, volatility refers to the degree of variation in stock prices over time, reflecting the uncertainty and risk investors face. According to the random walk hypothesis, these price movements are not only random but also unavoidable, as they result from countless unforeseen factors—ranging from economic news to geopolitical events—that can impact asset prices at any moment.

This inherent volatility makes it extremely difficult for investors to accurately predict future price movements or consistently outperform the market. The random walk theory argues that attempts to use technical analysis or market timing strategies are ultimately futile, since price changes do not follow any discernible pattern and are not influenced by past prices. Similarly, the efficient market hypothesis (EMH) supports this view by stating that asset prices reflect all available information, leaving no room for investors to gain an edge through analysis or prediction.

In the context of the stock market, volatility is often measured by indices such as the Dow Jones Industrial Average or the S&P 500, which track the price fluctuations of a broad set of stocks. While market volatility can be unsettling, investors can manage this risk by diversifying their portfolios and investing in broad market index funds. By spreading investments across a wide range of assets, investors can reduce the impact of random events on their overall returns and increase their chances of achieving long-term growth, even in the face of unpredictable price movements.

Random Walk Hypothesis and Its Critics

While the random walk hypothesis has shaped much of modern financial theory, it has also faced significant criticism from market practitioners and financial economists. Critics argue that the theory oversimplifies the complexities of financial markets by assuming that stock prices move purely at random, ignoring the influence of market participants’ behavior, economic policies, and other non-random factors.

For example, changes in interest rates, government regulations, and even market manipulation can all have a direct impact on market prices, challenging the idea that price movements are entirely random.

Technical analysts, in particular, dispute the random walk theory’s claim that past prices are irrelevant. They believe that historical price patterns and trends can provide valuable insights into future price movements, and many traders use technical indicators to inform their decisions.

Additionally, the success of renowned investors like Warren Buffett, who have consistently outperformed the market by focusing on company fundamentals, is often cited as evidence that stock picking and fundamental analysis can work, contradicting the random walk theory’s assumptions.

Despite these criticisms, proponents of the random walk hypothesis maintain that such examples are exceptions rather than the rule. They argue that most investors, over the long term, are unable to consistently outperform the market through stock picking or market timing.

According to the random walk theory, market prices are largely determined by random events, and any apparent patterns or successes are more likely due to chance than skill. As a result, the theory continues to serve as a foundational framework for understanding the unpredictable nature of financial markets and the challenges of consistently beating the market.

Random walk trading strategy backtest

In spreadsheets and trading programs, you can easily make a strategy that enters randomly. We use Amibroker to backtest (read our Amibroker review), and it takes just a couple of minutes to make a backtest with trading rules and settings. For this backtest, we analyzed historical price movements to evaluate the performance of the random walk strategy.

When reviewing the statistical results, it’s important to note that the random walk theory often assumes price changes follow a normal distribution, though real market data may deviate from this assumption.

We make the following trading rules for our random walk strategy backtest:

Trading Rules And Backtest

- We make 2-3 trades (buys) per month.

- Every buy is generated randomly.

- We exit after 5 trading days.

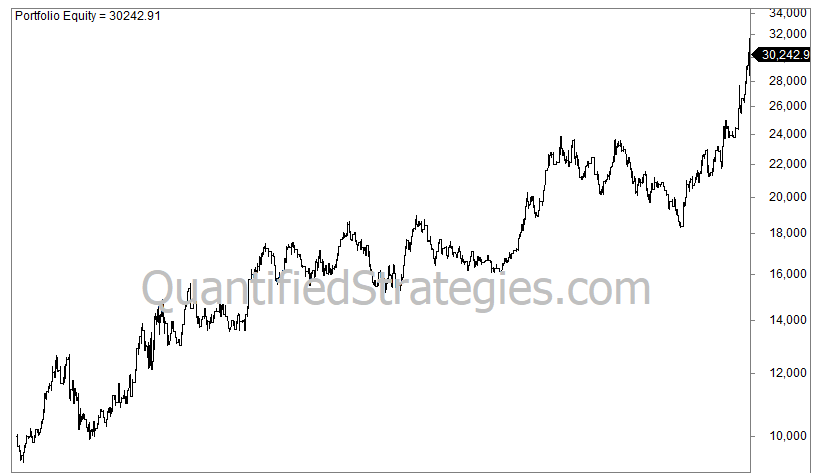

Our first backtest is done in stocks (S&P 500 – SPY). The equity curve looks like this:

Our random walk trading strategy performs pretty well on stocks (S&P 500) from 2003 to today.

The equity curve looks good, but the main reason is the tailwind from stocks. The trading statistics and historical performance metrics are good: The average gain per trade is 0.3%, the profit factor is 1.4 (profit factor example), and the max drawdown is 48%. The strategy’s annual return is 6.2%, but it’s invested only 45% of the time. If we adjust for that, the risk-adjusted return is almost 14%, which is better than buy-and-hold’s 11%.

All in all, not too bad for a completely random strategy.

Let’s make a second backtest on the gold price. To make it simple, we use the gold price ETF with the ticker code GLD.

The equity curve looks like this from its inception until today:

The 491 trades have an average of 0.25% per trade. It’s invested 45% of the time, and adjusted for that (11.6%), the return is the same as buy and hold.

Do you want trading code or the rules in plain English?

The Amibroker code for the random walk strategy can be purchased in our shop.

We have made our best free trading strategies and trading rules available for a small fee. If you are a Python trader, we believe our database is a potential goldmine (you can read more about Python trading – backtesting and examples). Additionally, all strategies come with code. For a full list of the 150 different strategies, please press the banner below.

Related reading: Random Entry Strategy and Random Walk Theory

Random walk trading strategy – ending remarks

Most of the price action in any financial market is random, thus making short-term trading difficult.

Luckily, there are still possibilities, and we believe the best route is what we are doing on this website: we make strict trading rules to quantify and backtest. If we find anything that works, we incubate it. If it is validated, we trade it live. You can read more about backtesting in our course:

We believe the best market to trade is the stock market. The reason is simple: you have an edge in the “constant” drift upward in the form of inflation and productivity gains. There is no coincidence that our random walk trading strategy managed to produce decent results simply by entering randomly.

It is also important to note that random walk theory has led to the rise of passive investment strategies, such as index investing, which aim to replicate the performance of the overall market rather than trying to outperform it through active management.

FAQ:

What is a Random Walk Theory trading strategy

Random Walk Theory in trading is the belief that stock market prices move unpredictably and exhibit a random character, meaning their movements are not influenced by past performance. The theory suggests that, due to this random character, fundamental or technical analysis cannot provide an advantage, as price changes are essentially “random,” making it impossible to consistently outperform the market using these methods.

How does a random walk trading strategy work?

The strategy involves diversifying risk across multiple stocks to mitigate losses from poorly performing stocks. The application of the random walk theory assumes a 50% probability of a stock price rising or falling at any given time.

By spreading investments across various stocks or using a broad market index fund, the strategy aims to take advantage of market randomness. Attempting to beat the market typically involves taking on additional risk, which the random walk theory does not recommend.

What are the rules for the random walk trading strategy?

The key rule is diversification, either by building a diversified portfolio of stocks across different industries or investing in a broad market index ETF. The random walk trading strategy is best suited for a long term investment strategy focused on diversification and passive investing. The strategy assumes a 50% probability of stock prices rising or falling, emphasizing passive investing and risk diversification.

How is the random walk theory related to the efficient market hypothesis (EMH)?

Both the random walk theory and EMH suggest that it is nearly impossible to consistently outperform the market. The concept of market efficiency is central to the efficient market hypothesis, which argues that asset prices already reflect all available information.

This high level of market efficiency means that even with new information, stock price movements remain unpredictable, making it difficult to find an edge in the market. While the random walk theory asserts that market movements are random, both theories support the idea that passive investing is often more effective than trying to beat the market through analysis or insider knowledge.